Ledoit-Wolf vs Covariance simple estimation¶

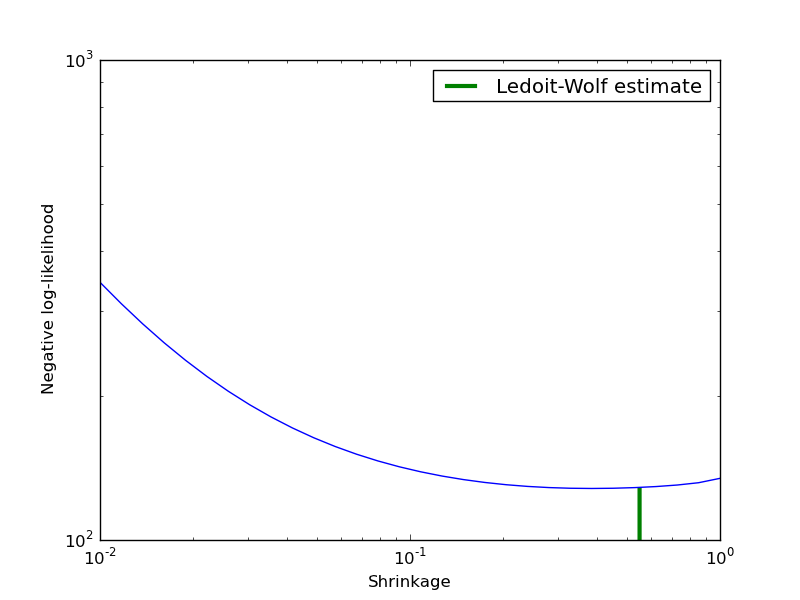

Covariance estimation can be regularized using a shrinkage parameter. Ledoit-Wolf estimates automatically this parameter. In this example, we compute the likelihood of unseen data for different values of the shrinkage parameter. The Ledoit-Wolf estimate reaches an almost optimal value.

Python source code: plot_covariance_estimation.py

print __doc__

import numpy as np

import pylab as pl

###############################################################################

# Generate sample data

n_features, n_samples = 30, 20

X_train = np.random.normal(size=(n_samples, n_features))

X_test = np.random.normal(size=(n_samples, n_features))

# Color samples

coloring_matrix = np.random.normal(size=(n_features, n_features))

X_train = np.dot(X_train, coloring_matrix)

X_test = np.dot(X_test, coloring_matrix)

###############################################################################

# Compute Ledoit-Wolf and Covariances on a grid of shrinkages

from scikits.learn.covariance import LedoitWolf, ShrunkCovariance

lw = LedoitWolf()

loglik_lw = lw.fit(X_train).score(X_test)

cov = ShrunkCovariance()

shrinkages = np.logspace(-2, 0, 30)

negative_logliks = [-cov.fit(X_train, shrinkage=s).score(X_test) \

for s in shrinkages]

###############################################################################

# Plot results

pl.close('all')

pl.loglog(shrinkages, negative_logliks)

pl.xlabel('Shrinkage')

pl.ylabel('Negative log-likelihood')

pl.vlines(lw.shrinkage_, pl.ylim()[0], -loglik_lw, color='g',

linewidth=3, label='Ledoit-Wolf estimate')

pl.legend()

pl.show()