Ridge Regression Variance Example¶

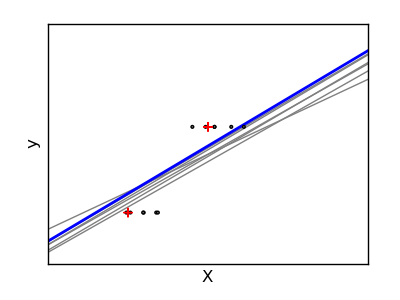

Ridge regression is basically minimizing a penalised version of the least-squared function. The penalising shrinks the value of the regression coefficients. Despite the few data points in each dimension, the slope of the prediction is much more stable and the variance in the line itself is greatly reduced, in comparison to that of the standard linear regression

Python source code: plot_ridge_variance.py

print __doc__

# Code source: Gael Varoqueux

# Modified for Documentation merge by Jaques Grobler

# License: BSD

import numpy as np

import pylab as pl

from sklearn import linear_model

X_train = np.c_[ .5, 1].T

y_train = [.5, 1]

X_test = np.c_[ 0, 2].T

fig = pl.figure(1, figsize=(4, 3))

pl.clf()

ax = pl.axes([.12, .12, .8, .8])

np.random.seed(0)

ridge = linear_model.Ridge(alpha=.1)

for _ in range(6):

this_X = .1*np.random.normal(size=(2, 1)) + X_train

ridge.fit(this_X, y_train)

ax.plot(X_test, ridge.predict(X_test), color='.5')

ax.scatter(this_X, y_train, s=3, c='.5', marker='o', zorder=10)

ridge.fit(X_train, y_train)

ax.plot(X_test, ridge.predict(X_test), linewidth=2, color='blue')

ax.scatter(X_train, y_train, s=30, c='r', marker='+', zorder=10)

ax.set_xticks(())

ax.set_yticks(())

ax.set_xlabel('X')

ax.set_ylabel('y')

ax.set_xlim(0, 2)

pl.show()